Share

BRISBANE, April 19, 2022 – In the third part of Monochrome’s “The Roads to an Australian Bitcoin ETF” series, the team explores the intricacies of European exchange-traded products (ETPs) holding crypto assets and the challenges faced by European regulators in bringing these products to market.

To understand the basis of the European experience with Bitcoin, one must first understand how European exchange markets are usually accessed, and why this makes ‘pure’ Bitcoin exposure via an Exchange-Traded Fund (ETF) far more complicated than it first may appear.

Due to different definitions of “crypto-asset” between Australian and European regulatory bodies it must be prefaced that we will be following Australian usage (with Bitcoin and Ethereum being the only two crypto currently considered “crypto-assets” as defined by the Australian Securities and Investments Commission). When referencing assets beyond Bitcoin and Ethereum, including as an umbrella or basket containing assets beyond, either “crypto” or “cryptocurrency” will be used.

The core hurdle for a Bitcoin ETF in Europe is the inability to use Undertakings for Collective Investment in Transferable Securities Directive (UCITS) as regulated vehicles exposed to single assets and the resulting need to use alternate product structures and the development of appropriate benchmarking for price discovery for this nascent digital asset class.

UCITS, Retail Suitability and Diversification

A concept unique to European markets, UCITS are a regulatory framework that creates a harmonised regime throughout Europe for the management and sale of pooled funds and by virtue of structure, ETFs. UCITS funds can be registered in Europe and sold to investors worldwide using unified regulatory and investor protection requirements. UCITS fund providers who meet the standards are exempt from national regulation in individual European Union member states. These funds are designed to be suitable for retail investors and their rules require certain levels of diversification to reduce vulnerabilities to performance from a small or single number of assets.

The most common restriction for UCITS is the ‘5/10/40 rule’. Broken down simply, this states that a maximum of 10% of a UCITS fund's net assets may be invested in securities from a single issuer, and that investments of more than 5 percent through a single issuer may not make up more than 40 percent of the whole portfolio.

The challenge for European ETP issuers seeking to offer listed products passively tracked to a single crypto-asset like Bitcoin was that they could not offer these assets within UCITS ETFs structures. The solution to the inability to launch a Bitcoin ETF in Europe would instead lie in alternate structured products, namely Exchange Traded Commodities (ETCs) and Exchange Traded Notes (ETNs).

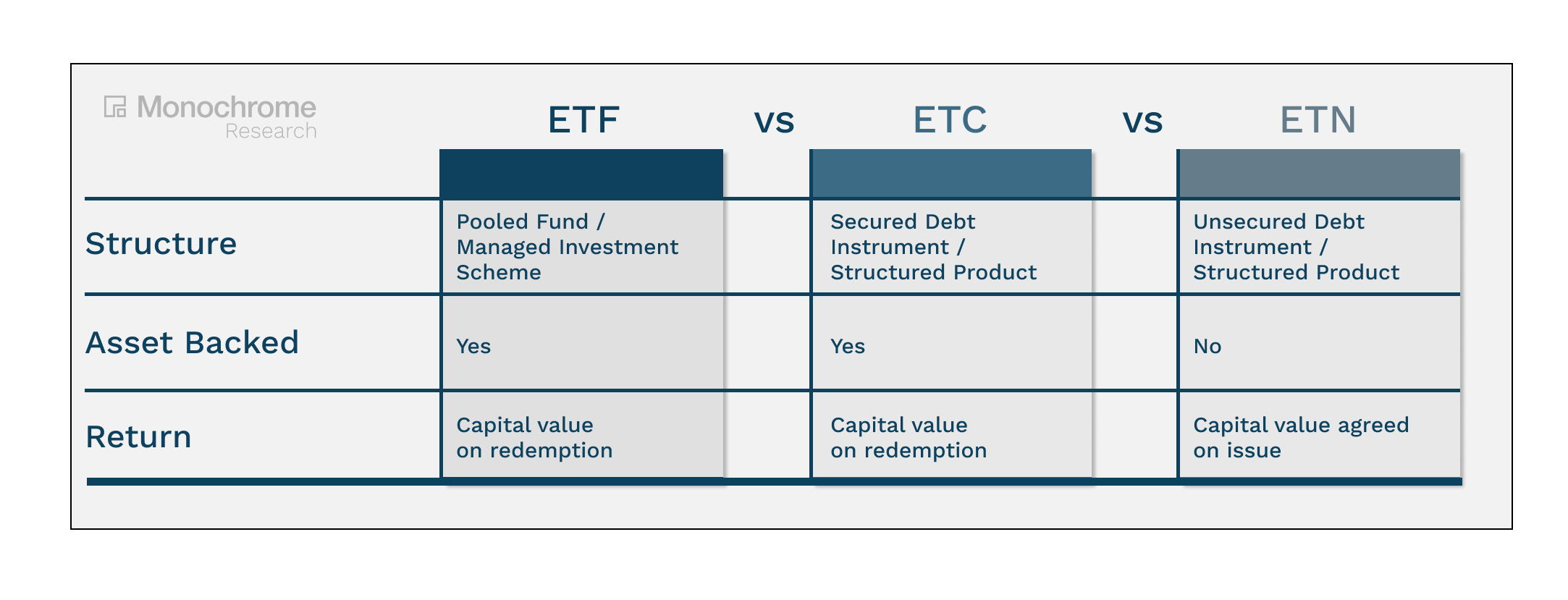

What is the difference? ETP vs ETF vs ETC vs ETN

Understanding the difference between product structures and the terminology associated helps to unpack the intricacy of European markets.

Beginning simply, ETPs are a broad umbrella term for any exchange traded product, whereas ETFs, ETCs and ETNs are specific types of ETPs.

Regarding underlying structure, ETFs are pooled funds (similar to managed investment schemes in Australia, whereas ETCs and ETNs are structured products. ETFs and ETCs are asset backed whereas ETNs are not, instead relying on the promise of the issuer to deliver the asset (or cash equivalent) on maturity.

Bitcoin, Crypto and the European Experience

European markets have been arguably one of the main champions for listed products holding both bitcoin and cryptocurrencies as a broad asset class.

However, because of diversification obligations underpinning UCITS ETFs preventing a ‘pure’ single asset Bitcoin ETF, European issuers turned to ETCs and ETNs as the most appropriate listed vehicles for retail exposure

Europe’s first Bitcoin ETC launched in June of 2020 on the Deutsche Börse’s Xetra exchange. The product, BTCetc - ETC Group Physical Bitcoin (BTCE), is issued by ETC Group and distributed by HANetf. It is a bond issue secured by underlying bitcoin. Currently, ETC Group also offers this ETC structured product to investors with a number of crypto options beyond bitcoin and ether.

As of April 6, 2022, BTCE has approximately US $888 billion in assets under management, currently being the most liquid product available in European markets and most traded ETP on the Deutsche Börse Xetra in 2021, demonstrating considerable investor appetite for the asset class regardless of product form.

Such an extended offering contrasts with the Australian market where pooled funds are not subject to diversification obligations, although perhaps in part because of this, the regulator has limited appropriate underlying crypto assets to just bitcoin and ether as per ASIC Report 705.

Following the launch of BTCE, ETC Group would introduce an ETN product known as Bitcoin ETN Futures (FBTX). FBTX launched on September 13, 2021 on Eurex, Europe’s largest derivatives exchange, offering futures contracts for BTCE at a predetermined price but not secured by the physical bitcoin. Instead, the futures contracts are satisfied by the physical delivery of BTCE securities on maturity.

This engagement via ETNs and ETCs has extended beyond just bitcoin offerings, with upwards of 70 crypto ETPs currently available across Europe.

Price Discovery in Europe, Benchmarking and Global Implications

As global markets looked to introduce regulated onramps for crypto exposure, several notable hurdles emerged, with the likes of asset classification (see part 2 of our series here) and futures versus spot (see part 1 of our series here) being crucial to some markets. Another key focus of regulators was establishing robust benchmarking to meet regulator demands for market transparency.

This has also been a key protection measure for Australian retail investors, with the Australian Securities and Investment Commission (ASIC) in INFO 230 pointing to compliance with recognised benchmark selection principles such as the International Organization of Securities Commissions (IOSCO) Principles for financial benchmarks, the UK Financial Control Authority (FCA) Benchmark Regulation and the EU Benchmarks Regulation (EU BMR) as a key prerequisite of retail crypto-asset product approval.

In August 2019, CF Benchmarks became the first crypto-asset index provider to be authorised by the FCA as a Benchmark Administrator under the EU BMR, thus opening the door for EU ETPs exposed to cryptocurrencies tracked against reliable and transparent indexes.

In January 2020 the EU BMR passed a key transition period, with benchmarks established prior to 2018 now requiring compliance with updated standards previously only required for benchmarks established after the update. By closing this transition period for updated compliance standards, consistent standards were cemented for all EU-based index tracking products.

Increased Regulation Equals Increased Adoption?

Executive Vice-President of the European Commission, Valdis Dombrovskis, stated in 2019 at his confirmation hearing before the European Parliament that he intended to propose a legislative framework that would cover all cryptocurrencies, including ‘stablecoins’, to ensure legal certainty for both innovators and investors. At the same time this legislative framework would aim to address consumer risks, as well as risks to market integrity, market fragmentation and financial stability.

In doing so, he sent a clear message to European markets that engagement with the nascent asset class was imminent.

Subsequent changes to MiFID II - the legislative framework used by the EU to regulate financial markets in the bloc and improve consumer protections - encouraged a technology-neutral definition of financial instruments so that instruments based on blockchain technology fall within the definition of ‘financial instrument’ if they relate to securities, money market instruments, options, futures, swaps, future interest rate agreements and any other derivatives agreement relating to the securities.

In other words, the change in MiFID II clarifies that it is not the actual form of issuance, but the purpose of the issuance, that determines whether an issue is a financial instrument or not.

More significantly, on 24 September 2020, the EU Commission published a proposal for the regulation of EU-defined crypto - the ‘Markets in Crypto-Assets Regulation’ (MiCA). Once adopted, MiCA will apply to all EU member states and will regulate all issuers and service providers dealing with crypto. It will require issuers and service providers of services based on cryptocurrencies - e.g. custody, brokerage, trading, or investment advice - to have specific cryptocurrency authorisations from national regulators.

Finally, on 14 March 2022, the EU Parliament voted against banning proof-of-work in a proposed bill on crypto regulation in the bloc. This provided a clear signal on intent by the EU in relation to the adoption of crypto within its regulatory frameworks.

Bringing it Back Home to a Bitcoin ETF in Australia

With the European experience now front of mind, Australian investors following along may be curious to how this factors into the market that matters most for them.

In part 4 of this series, we will dissect the intricacies of Australian regulation and the challenges of the Australian market in bringing listed financial products holding this nascent asset class to market.

Join Monochrome’s mailing list for notification of part 4 and more. Access the other parts below.

The content, presentations and discussion topics covered in this material are intended for licensed financial advisers and institutional clients only and are not intended for use by retail clients. No representation, warranty or undertaking is given or made in relation to the accuracy or completeness of the information presented. Except for any liability which cannot be excluded, Monochrome, its directors, officers, employees and agents disclaim all liability for any error or inaccuracy in this material or any loss or damage suffered by any person as a consequence of relying upon it. Monochrome advises that the views expressed in this material are not necessarily those of Monochrome or of any organisation Monochrome is associated with. Monochrome does not purport to provide legal or other expert advice in this material and if any such advice is required, you should obtain the services of a suitably qualified professional.

Related Articles

Your Complete Guide to the Australian Bitcoin ETFs Functionality

This comparison breaks down two game-changing features: bitcoin deposit and withdrawal flexibility (can you actually move Bitcoin in and out of the ETF?) and fund structure (do you truly own the Bitcoin?). These distinctions might seem technical, but they have real implications for your investment strategy, tax treatment, SMSF reporting, and long-term flexibility.